All Categories

Featured

Table of Contents

At the end of the day you are acquiring an insurance item. We like the defense that insurance supplies, which can be gotten much less expensively from an affordable term life insurance coverage plan. Overdue financings from the policy might additionally reduce your survivor benefit, diminishing one more level of security in the plan.

The concept only works when you not just pay the substantial costs, yet make use of added cash to buy paid-up enhancements. The possibility price of all of those dollars is tremendous very so when you could instead be purchasing a Roth Individual Retirement Account, HSA, or 401(k). Even when contrasted to a taxed financial investment account or perhaps an interest-bearing account, infinite financial might not offer comparable returns (contrasted to investing) and comparable liquidity, access, and low/no charge structure (compared to a high-yield financial savings account).

When it comes to financial preparation, whole life insurance often stands out as a prominent option. While the concept could appear attractive, it's essential to dig much deeper to comprehend what this truly indicates and why watching whole life insurance coverage in this way can be misleading.

The concept of "being your very own bank" is appealing due to the fact that it recommends a high degree of control over your funds. This control can be imaginary. Insurance companies have the supreme say in exactly how your plan is managed, including the regards to the financings and the prices of return on your cash money worth.

If you're taking into consideration entire life insurance policy, it's crucial to view it in a wider context. Whole life insurance policy can be an important tool for estate preparation, supplying an assured death advantage to your recipients and potentially supplying tax benefits. It can also be a forced savings vehicle for those that have a hard time to conserve money consistently.

It's a kind of insurance policy with a financial savings element. While it can supply steady, low-risk growth of cash money value, the returns are generally less than what you might attain with other financial investment cars (rbc infinite visa private banking). Before leaping right into whole life insurance with the concept of boundless banking in mind, make the effort to consider your financial goals, risk resistance, and the complete array of economic products readily available to you

Infinite Banking Solution

Infinite financial is not a monetary panacea. While it can operate in particular circumstances, it's not without threats, and it calls for a considerable dedication and recognizing to manage properly. By recognizing the potential pitfalls and understanding the real nature of entire life insurance policy, you'll be much better furnished to make an enlightened choice that sustains your economic health.

This book will certainly teach you exactly how to establish a banking policy and exactly how to make use of the financial policy to purchase property.

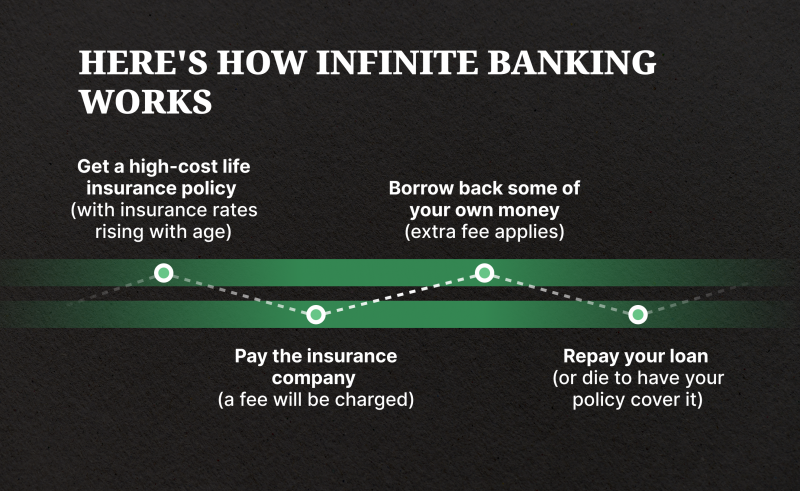

Infinite banking is not a services or product offered by a specific establishment. Infinite banking is a technique in which you acquire a life insurance policy policy that gathers interest-earning money value and obtain finances against it, "borrowing from yourself" as a resource of resources. Then at some point repay the funding and begin the cycle throughout again.

Pay policy costs, a section of which builds cash value. Take a financing out against the plan's cash value, tax-free. If you utilize this concept as meant, you're taking cash out of your life insurance policy to purchase whatever you would certainly need for the rest of your life.

The are whole life insurance coverage and universal life insurance policy. The cash money worth is not included to the death advantage.

After one decade, the cash worth has actually grown to about $150,000. He takes out a tax-free funding of $50,000 to start a business with his bro. The plan finance passion price is 6%. He pays off the lending over the following 5 years. Going this route, the rate of interest he pays goes back into his policy's money worth instead of a banks.

Infinite Income Plan

Nash was a financing specialist and follower of the Austrian school of business economics, which advocates that the value of goods aren't clearly the result of typical economic frameworks like supply and need. Rather, people value cash and products in different ways based on their financial status and demands.

One of the risks of typical financial, according to Nash, was high-interest prices on loans. Long as banks established the interest prices and financing terms, people didn't have control over their very own wide range.

Infinite Banking requires you to have your financial future. For goal-oriented individuals, it can be the best economic tool ever before. Below are the advantages of Infinite Financial: Arguably the solitary most helpful facet of Infinite Banking is that it improves your cash money circulation.

Dividend-paying whole life insurance is very low risk and provides you, the insurance policy holder, a good deal of control. The control that Infinite Banking offers can best be organized right into 2 categories: tax obligation advantages and asset securities. Among the factors entire life insurance is ideal for Infinite Banking is how it's exhausted.

When you make use of whole life insurance policy for Infinite Banking, you get in right into an exclusive contract in between you and your insurance coverage business. These securities might differ from state to state, they can consist of defense from property searches and seizures, protection from reasonings and defense from creditors.

Entire life insurance coverage plans are non-correlated properties. This is why they work so well as the monetary structure of Infinite Banking. No matter of what occurs in the market (stock, actual estate, or otherwise), your insurance coverage plan maintains its well worth.

How Infinite Banking Works

Entire life insurance is that third bucket. Not just is the rate of return on your entire life insurance plan ensured, your fatality advantage and premiums are likewise guaranteed.

Right here are its main advantages: Liquidity and availability: Policy fundings offer immediate access to funds without the restrictions of standard financial institution financings. Tax efficiency: The cash value grows tax-deferred, and policy loans are tax-free, making it a tax-efficient tool for building wide range.

Asset defense: In lots of states, the money worth of life insurance policy is protected from financial institutions, adding an added layer of monetary safety and security. While Infinite Financial has its advantages, it isn't a one-size-fits-all service, and it comes with considerable disadvantages. Below's why it may not be the best approach: Infinite Banking typically needs detailed policy structuring, which can puzzle insurance holders.

Envision never having to fret about small business loan or high rates of interest once more. Suppose you could borrow cash on your terms and develop wide range all at once? That's the power of limitless financial life insurance policy. By leveraging the money value of whole life insurance IUL plans, you can grow your wealth and borrow cash without depending on conventional financial institutions.

There's no collection loan term, and you have the freedom to pick the payment schedule, which can be as leisurely as settling the car loan at the time of death. This versatility encompasses the maintenance of the car loans, where you can go with interest-only settlements, keeping the car loan balance level and workable.

Holding money in an IUL dealt with account being credited passion can typically be far better than holding the cash on down payment at a bank.: You've always desired for opening your own bakery. You can obtain from your IUL plan to cover the preliminary expenses of renting a room, buying devices, and working with team.

Build Your Own Bank

Individual lendings can be obtained from conventional financial institutions and credit score unions. Borrowing money on a credit report card is generally very pricey with yearly portion rates of interest (APR) typically reaching 20% to 30% or more a year.

The tax obligation therapy of policy finances can vary considerably depending upon your country of residence and the details regards to your IUL policy. In some areas, such as The United States and Canada, the United Arab Emirates, and Saudi Arabia, policy finances are typically tax-free, using a significant advantage. Nevertheless, in various other jurisdictions, there may be tax obligation ramifications to consider, such as possible tax obligations on the lending.

Term life insurance policy only gives a survivor benefit, without any kind of money worth build-up. This suggests there's no cash money worth to borrow versus. This write-up is authored by Carlton Crabbe, Chief Executive Officer of Resources for Life, an expert in offering indexed global life insurance policy accounts. The info supplied in this write-up is for academic and informative functions just and should not be interpreted as monetary or financial investment recommendations.

Nevertheless, for financing police officers, the comprehensive guidelines enforced by the CFPB can be viewed as cumbersome and limiting. Loan policemans often say that the CFPB's guidelines develop unneeded red tape, leading to even more paperwork and slower financing processing. Regulations like the TILA-RESPA Integrated Disclosure (TRID) regulation and the Ability-to-Repay (ATR) requirements, while intended at securing consumers, can bring about delays in shutting bargains and increased operational costs.

{kind=link}

Latest Posts

How Do I Start Infinite Banking

Become Your Own Bank. Infinite Banking

Using A Life Insurance Policy As A Bank